OIL REPORT

JANUARY 1ST TO 20TH, 2021

PRICE

Oil prices began the year on the rise, with Brent and WTI prices rising 13% and 14% respectively in the first two weeks of the year when prices were increasing from $50.08 and $47.02 a barrel to $56.55 and $53.71 a barrel as of January 20th, respectively.

A higher demand produces this price increase, explained by the coming into force, on January 1st, of the OPEC+ decision of last December, to increase its production by 500 MBD and the beginning of the massive vaccinations against COVID-19 in the USA, the United Kingdom, and Europe.

However, what gave additional impetus to the price rise during the first half of the month was the announcement on January 4th by the Kingdom of Saudi Arabia of a cut, additional to those stipulated in the OPEC+ agreements, of 1 million barrels a day of production for February and March. This announcement, which took both market operators and the OPEC+ countries themselves by surprise, brought the quotations of both the Brent and the WTI to maximum levels from February 20th, 2020.

PRICE IMPULSE GIVEN BY THE

SAUDI ARABIA CLIPPING ANNOUNCEMENT

The Saudis’ unilateral production cut seems to reflect the Kingdom’s intention to reassert its leadership in the conduct of the oil market and compensate for the additional production increase agreed by OPEC+ in favor of Russia and Kazakhstan, as well as the rise in Libyan production.

On the other hand, prices have also been underpinned by the draining of worldwide crude oil inventories. According to the STEO report from the Energy Information Administration (EIA), published on January 12th, between June and December were reduced by 0.5 million barrels a day, and in the U.S., which has been greater than expected, when as of January 8th, they drained 11 million barrels a day in comparison with the closing of 2020, according to data provided by the EIA on January 6th.

OIL PRICE BEHAVIOR

BRENT AND WTI

(Dec 2020 — Jan 2021)

Source: Bloomberg data. Own elaboration.

Although these elements are reflected in the strengthening of market fundamentals, demand uncertainty continues to affect prices, mainly due to the substantial increase in COVID-19 infections worldwide, particularly in the United States, the United Kingdom, Europe, and Brazil.

The consequences of the “second wave” of infections in 2020, and the measures to contain an imminent “third wave” in 2021, have led to the tightening of Europe and the United Kingdom’s health measures and the application of strict restrictions on mobility. All of the above will be in force until the end of the first quarter of 2021, now accompanied by the new U.S. administration measures, which has promised a more active role in tackling the pandemic in that country.

On the other hand, there are significant concerns about the virus’s mutations and the complications that the complex process of massive vaccinations initiated in the U.S., U.K., and Europe. The reasons are the insufficient number of vaccines and the urgency of the most affected developed countries pressing for greater quantities with priority, and the cold logistics that Pfizer and Moderna vaccines require.

On Friday, January 15th, the Brent and WTI indicators closed down to $55.56 and $52.82 a barrel, following China’s announcement on January 14th that it had reported the largest increase in Covid-19 infections in the last ten months and had taken new mass containment measures.

This fall was picked up by the scoreboards in the week of January 19–21 as a positive market reaction to the entry into office of the new U.S. administration and President Joe Biden’s swearing-in, signifying a significant degree of political stability in the world’s leading economic-military power.

The differential between the Brent and WTI markers continues to widen concerning the differential between March and October. This week, they ranged between 3.5 and 3.3 dollars a barrel, although this increase is still below the differential recorded in January 2020, of 8 dollars a barrel.

OPEC Basket

The OPEC basket maintains the upward trend of the last quarter of 2020 and shows an increase of 8% as of January 20th, 2021, to $55.75 per barrel.

PRICE OF THE OPEP BASKET

(October-December 2020)

Source: Organization of Petroleum Exporting Countries

Among the crudes that make up the OPEC basket, at the close of 2020, those that show the highest price, above 42 dollars a barrel, are Murban, Sunflower, and Saharan Blend crudes. The rest fluctuates at an average of 41 dollars a barrel, although the heavy Djeno and Merey crudes average well below, at 35.77 and 28.12 dollars a barrel, respectively.

PRODUCTION

Between January 4th and 5th, was held the ministerial meeting of the OPEC+ countries. They ratified the decision taken last December to increase production by 500 thousand barrels as of January this year, recognizing that the “fragility” of the economic recovery in 2020 will be transferred to 2021 because of “the increase in infections, the return of stricter blockade measures and the growing uncertainties.”

After confirming the production increase agreed in December, an additional production increase of 65 thousand and 10 thousand barrels of oil per day was decided for Russia and Kazakhstan, respectively, for February and March.

The increase in the OPEC+ production quota in January will be 500 thousand barrels per day. In February, it will be 575 thousand barrels per day and 650 thousand barrels per day in March, with the extra production from Russia and Kazakhstan.

The Saudi decision

Immediately after the OPEC+ ministerial meeting, on January 5th, Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, announced that the Saudi Kingdom had decided to make a voluntary, unilateral cut oil production by 1 million barrels a day for February and March. The announcement came on top of the 1,881 MMBD cut quota agreed earlier that day, increasing its cut to 2,881 MMBD for the next two months and placing the Saudi production quota at 8,119 MMBD.

This decision by Saudi Arabia surprised OPEC+ and the world market, causing the oil price to rise by 5%, while allowing the state-owned Saudi ARAMCO, on January 6th, to increase the Arabia Light for clients in Asia by 70 cents and by 20 cents for the U.S. market.

There is much speculation about this decision’s origin; however, there are fascinating aspects to highlight, beyond the real motivations, that impact the oil market actors.

It is noteworthy that this cutback is a sign of strength towards OPEC+ and the world market, as it does not involve the other Gulf monarchies — Kuwait and UAE — as it was in May last year. This fact shows the internal differences around the cutback policy and the need to expand production, especially according to the UAE and the Abu Dhabi National Oil Corporation (ADNOC).

The second interesting aspect is that Saudi Arabia demonstrates that it can impact the market with its decisions, even though Russia and the rest of the Gulf producers, especially the UAE, do not share the same vision and need to increase their production. Saudi Arabia is sending a clear signal of its determination and capacity to influence the market and impose its policy on OPEC and OPEC+.

The Saudi minister described the cut as a “sovereign political decision” by Crown Prince Mohammed bin Salman to “support our economy, the economies of our colleagues in OPEC+ countries and industry.”

Russian Deputy Prime Minister Alexander Novak defined the Saudi decision as “a new year’s gift” for the oil sector, a “gift” that only the Saudi minister and the Crown Prince knew about.

The Saudi decision seems to be more of a geopolitical consideration of Crown Prince Mohamed bin Salman, offering help to American producers, especially to the big companies that are partners of Saudi Aramco, and to the new administration that will take office next January 20th. On the same day, the announcement was made that the Crown Prince received the Emir of Qatar, Tamim bin Hamad al-Thani, at the 41st Summit of the Gulf Cooperation Council. In this way, they establish the end of the confrontation between the two monarchies and the easing of tensions between the American allies in the Persian Gulf, an element that the new American administration will indeed consider.

Simultaneously, the Saudi announcement counteracts other countries within OPEC+, such as Russia and the UAE, of not creating price conditions that would allow the recovery of production and the market for U.S. shale oil producers.

The most favored with the current price level of over $45–50 a barrel are the American oil producers, which created unrest in the United Arab Emirates. This Gulf country is not comfortable with the possibility of U.S. oil “flooding the market.”

The UAE’s energy minister, Suhail Mohamed Al Mazrouei, expressed his concern in this regard. In an interview at the Gulf Intelligence forum, held on January 13th, referring to the American shale oil producers, he warned that “it is prudent not to raise the weapon and produce excessively during the year of recovery.”

Finally, the Saudi decision has been consistent to restrict oil supplies, forcing excess inventory drainage.

Deputy Prime Minister Novak, who at the OPEC+ meeting requested the group to increase the production quota by 500 thousand barrels a day in February and March, recognized that the Saudi decision should generate faster drainage of the crude oil inventories so that they return to their “normal levels,” one of the inconveniences that put the stability of the oil market at risk.

This goal explains how Saudi Aramco’s exports to the U.S. fell to zero the week of December 28th, 2020, which had not happened since 1985. The Saudi minister described it as a “commercial decision” rather than a political one.

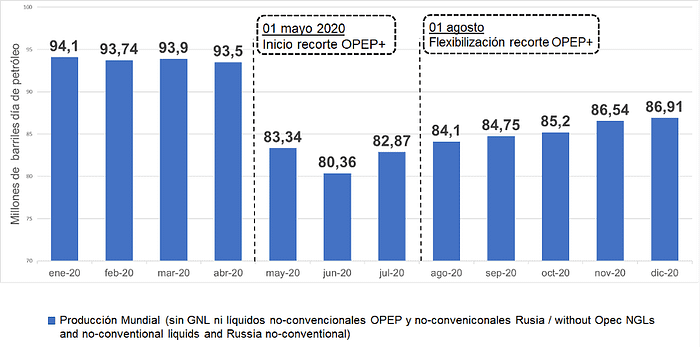

World oil production.

December 2020 closed with a world oil production of 86.91 MMBD, according to data published in the OPEC Monthly Oil Market Report of January 14th and the Russian Ministry of Energy. This is the highest level since the production cut began in May 2020.

This rise represents an increase of 370 thousand barrels per day compared to November, of which 340 thousand barrels per day corresponds to OPEC+, highlighting the production increase in Libya.

For the first quarter of 2021, world oil production is expected to remain similar until December. The increase of OPEC+ output — between 500 MBD and 650 MBD between January and March — and Libya’s production will be off-set by Saudi Arabia’s 1 million barrel a day oil cut.

In this way, the first quarter of the year will allow us to reach a floor of greater market stability and recovery of the price, keeping the oil supply regulated to continue draining inventories as the supply of COVID-19 vaccines advances and demand gradually recovers.

WORLD OIL PRODUCTION 2020

(January — December)

Source: Own elaboration with data from the MORM OPEP of January 2021.

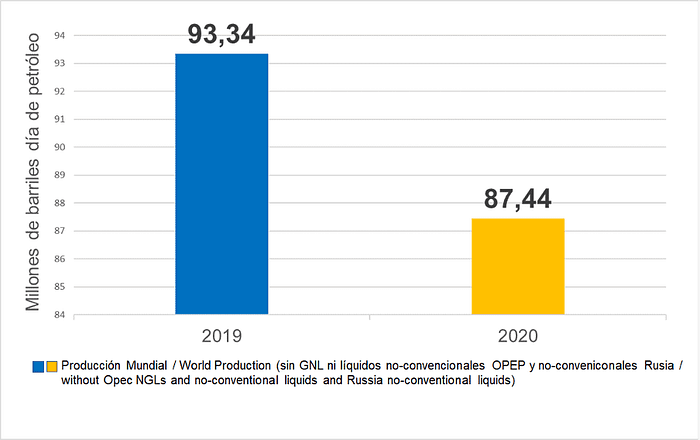

According to OPEC data, average world oil production in 2020 stood at 87.44 million barrels per day, which is 5.9 million barrels per day less than in 2019, and a year-on-year drop of 6.3%.

U.S. Energy Information Administration data (EIA) shows an average global oil production of 89.26 MMBD in 2020. In its January 19th report, the International Energy Agency (IEA) reports production of 92.8 MMBD in December 2020.

WORLD OIL PRODUCTION 2019–2020

Source: Own elaboration with OPEC data.

Both the EIA and the IEA estimate that oil production had a year-on-year decrease of 6 MMBD in 2020, not far from OPEC’s data, representing a drop of 6.3%.

This decrease in world oil production in 2020 reflects the effort to cut production agreed by OPEC+ since last May, as well as the fall in oil production in the U.S. In this way, a record of a year of outstanding efforts for the producing countries, by complying with the policy of production cuts and regulating the oil market to defend the value of oil, is an exhaustible strategic natural resource.

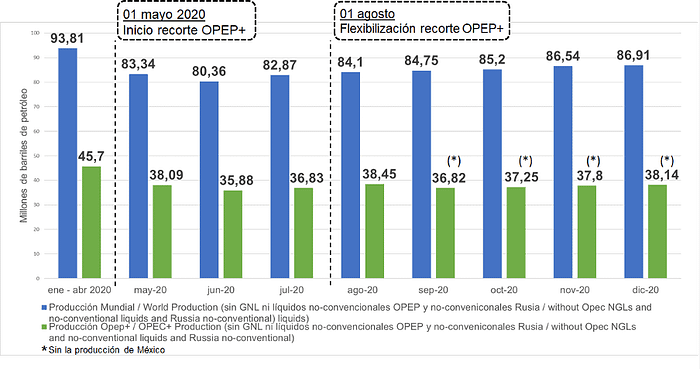

OPEC+ oil production

Of the world oil production at the end of 2020–86.91 million barrels a day, the highest in 8 months — 43.9% of it, equivalent to 38.14 million barrels a day, corresponds to the countries’ production grouped in OPEC+.

WORLD OIL PRODUCTION / OPEC+ (January-December 2020)

Source: Own elaboration with data from the MORM OPEP of January 2021, Russian Ministry of Energy, Azerbaijan Ministry of Energy, PEMEX, and S&P Global Platts

Of OPEC+ production, 25.36 MMBD correspond to OPEC and 12.78 MMBD to non-OPEC, equivalent to 66.5% and 33.5% of the group’s output.

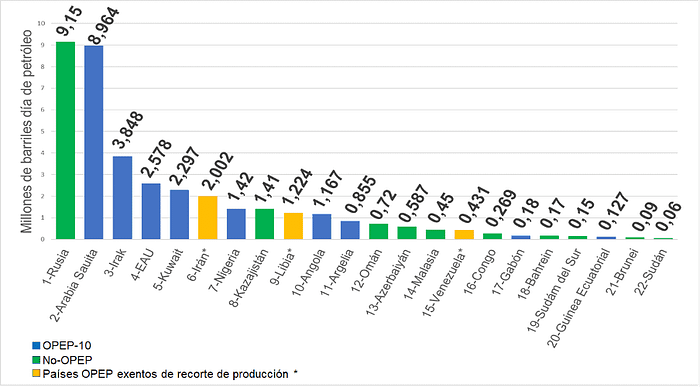

OPEP+ PRODUCTION RANKING

(December 2020)

Source: Own elaboration with MORM OPEP data January 2021, Ministry of Energy of Russia, Ministry of Energy of Azerbaijan, and S&P Global Platts

- OPEC Production

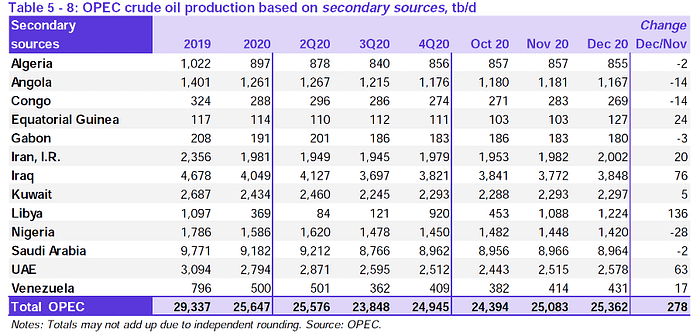

Regarding OPEC, the members that agreed to reduce their production on April 12th, OPEC-10 (Algeria, Angola, Congo, Equatorial Guinea, Gabon, Iraq, Kuwait, Nigeria, Saudi Arabia, and the United Arab Emirates), reached 21.7 MMBD, equivalent to 56.9% of the OPEC+ output, 25% of world production and 85.6% of OPEC production.

OIL PRODUCTION OF OPEC COUNTRIES ACCORDING TO SECONDARY SOURCES

(December 2020)

Source: MORM OPEC January 2021

Iraq’s production stands out, with 3,848 MMBD, an increase of 2%, to the previous month, 76 thousand barrels a day of oil, not meeting its production cut quota for the first time since July 2020. This level of production is within the quota from January 2021 of 3,857 MMBD, coinciding with the January 11th resumption of activities in the Salahuddin/2 sector of the Baiji refinery, the biggest in Iraq — destroyed21 by the DESA in 2014 — setting the production of refined products in Baiji from 70 thousand to 140 thousand barrels a day.

The United Arab Emirates increased its production by 63,000 barrels of oil per day, while Gabon and Equatorial Guinea increased their outputs by 24,000 barrels per day.

On the other hand, Angola — whose Minister, Diamantino Pedro Azevedo, is presiding over this year’s OPEC Conference — continued to respect its commitment to compensate for their 2020’s overproduction, with a new decrease in its production; this time, of 14 thousand barrels of oil per day. The same happened in Nigeria, with a reduction of 26,000 barrels of oil per day.

Regarding the three OPEC countries exempt from production cuts (Iran, Libya, and Venezuela), they produced together 3,657 MMBD of oil, of which 3,226 MMBD, 88.2%, corresponding to Iran and Libya. At the same time, Venezuela continues to be affected by the government’s inability to manage the oil sector, which is reflected in the production of only 431 thousand barrels of oil per day.

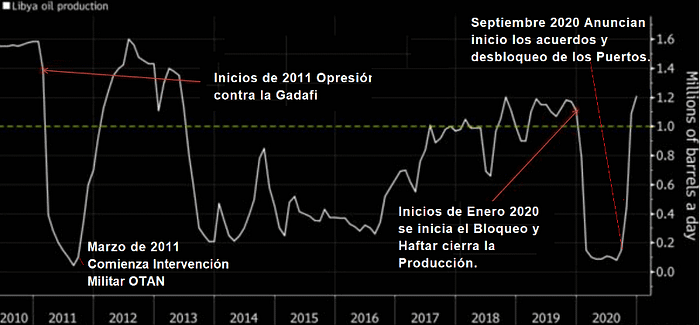

The situation in Libya

Libya presented a production of 1,224 MMBD of barrels per day in December 2020 — its highest level since May 2013 — continuing the rise registered since Khalifa Haftar, leader of the Libyan National Army and the Parliament of Tobruk, announced, on September 18th, 2020, the resumption of oil activities as a result of the agreement signed on December 17th, 2015, and supported by the U.N. to form a “national unity” government.

As of October 26, 3 days after the ceasefire agreement, the NOC announced “the total end of the blockades in all fields and ports,” reactivating operations to bring production above one million barrels of oil. The above has been reflected in Libyan production’s remarkable recovery, which increased from 84 thousand barrels a day in the second quarter of 2020 to 1,224 million barrels a day in December, a recovery of 1357% in 6 months.

However, on January 17th, 2021, the National Oil Corporation (NOC) reported the need to halt the Waha Oil Company pipeline’s operations, which carries oil from the Samah-Dhara area to the Esseder terminal. This stoppage reduces the country’s production by 200 MBD and means that from that date, production was 1 MMBD.

According to NOC spokespersons, the suspension of operations on the pipeline is due to the need to carry out major maintenance work that cannot be postponed because of the pipeline’s innumerable leaks. The above is an example of the problems that continue to affect confidence in the country’s production after the military intervention that overthrew Muammar Gaddafi’s government.

The Libyan oil industry’s reliability problems are related to the permanent military conflicts and ungovernability that have plagued the country since then and to the delay in the country’s production infrastructure’s maintenance and repair works during the war.

However, this situation does not prevent the country with the largest oil reserves in Africa from increasing its production levels, as it has been doing since October 2020.

LIBYA’S OIL PRODUCTION

(2010–2020)

Source: Bloomberg, own elaboration

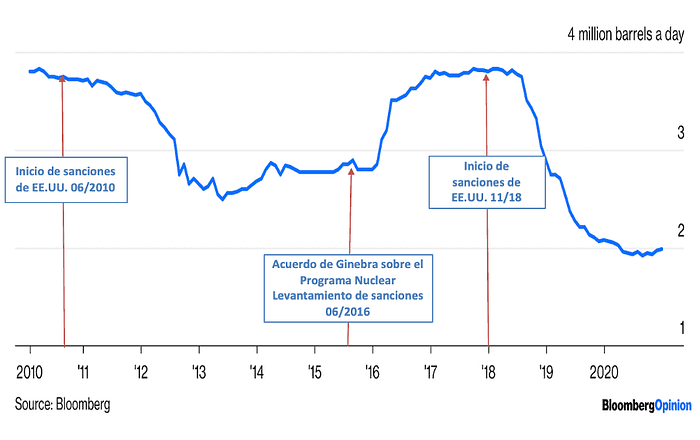

The situation in Iran

In Iran’s case, with a production of 2 million barrels of oil per day in December, there is the expectation that diplomatic negotiations will be resumed with the new U.S. administration that takes up office on January 20th.

President-elect Joe Biden has stated his intention to resume the nuclear agreement with Iran, the P6+1 deal, reached in July 2015 at the U.N. Security Council, which led to the lifting of U.S. sanctions in January 2016 during the Obama administration. These agreements were abandoned in May 2018 by the Trump administration, which in November 2018 again imposed sanctions on the Persian nation, affecting the oil sector in particular.

Iran, a founding member of the EPO and a key country in the supply of oil and gas to Europe, India, and China, has demonstrated its capacity to re-establish its oil production as soon as the U.S. sanctions ceased. This recovery is similar to the situation experienced in 2016 when Iran recovered its production by 900,000 barrels per day in 6 months.

If the U.S. sanctions are lifted as a result of a rapid negotiation process between the Biden administration and Iran, the latter could increase its production by at least 500 thousand barrels a day in three months (as it did in April 2016), on a path to recover 1.8 MMBD and regain it 3.8 MMBD production it had in June 2018; this would change the correlation of forces within OPEC+.

IMPACT OF U.S. SANCTIONS ON

IRAN’S OIL PRODUCTION

(2010–2020)

Source: Bloomberg, own elaboration

Iran, whose production in 2004 was 4 MMBD, with reserves of 208.6 billion barrels of oil and 895.6 TCF (trillion cubic feet) of gas, constitutes one of the most important world oil and gas suppliers. U.S. sanctions brought its oil production to 2.8 MMBD in 2015; however, once the Obama administration lifted the sanctions on January 17th, 2016, Iran was able to increase its production to 3.8 million barrels per day in 12 months.

In June 2016, Iranian oil production reached 3.7 million barrels per day. A 32% increase in just six months, levels that it maintained throughout 2017 and part of 2018 and until the US Trump administration again imposed sanctions on the Persian country; as a result, its production fell to 2.1 million barrels per day at the end of 2019, and it reached 2 million barrels per day at the end of 2020.

The motives of the U.S. or the Trump administration to re-impose sanctions on Iran in November 2018 are in response to the aggressive strategy of the Middle East’s outgoing administration. This is characterized by its unrestricted support for Israel, both in its policy of annexing the Palestinian territories and its confrontation with Iran, seeking to weaken it and “contain” it in the region. Also, by giving in to pressure from Israel itself and to the Persian Gulf monarchies’ demands, fundamentally Saudi Arabia and the UAE, to re-impose sanctions on Iran.

The Trump administration has tried, without success, to get the U.N. Security Council to join it in its sanctions against Iran. In August 2020, as he participated in the Council, outgoing Secretary of State Mike Pompeo advocated re-imposing U.N. sanctions on Iran. None of the countries that signed the 2015 nuclear agreement with Iran joined the Trump administration in its purpose. Iran has rigorously complied with the nuclear agreement, as confirmed by the Security Council and the International Atomic Energy Agency (IAEA). Also, Iran has historically been an oil supplier to China, India, and Europe.

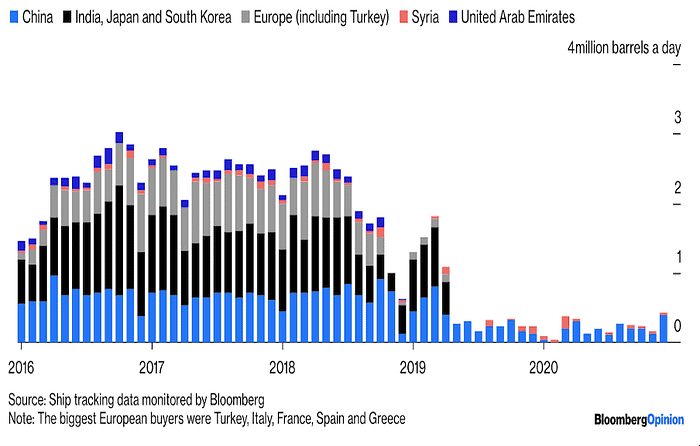

The outgoing U.S. administration sanctions directly hit Iran, thus supporting its interests in the Persian Gulf and affecting the supply of oil to Asian economies, particularly to China, given the increasingly hostile relationship.

COUNTRIES AFFECTED BY THE DECLINE IN OIL SUPPLIES FROM IRAN AS A RESULT OF U.S. SANCTIONS

(2016–2020)

Source: Bloomberg

For the Biden administration, resuming diplomatic negotiations with Iran is now much more complicated than during the Obama administration, since geopolitical conditions have changed since 2015.

The aggressive attitude of the Trump administration against Iran and its disregard for the nuclear agreement of 2015, including the assassination of the general of the Revolutionary Guard of Iran, Qasem Soleimani, on January 3rd, 2020, in a drone attack in Iraq, has provoked the intensification of the already historical distrust of the political and religious sectors of Iran towards the U.S. It has also weakened the Iranian president’s position, Hasan Rohani, the 2015 nuclear agreement architect, regarding the next Iranian elections on June 18th, 2021.

As a direct consequence of the U.S. withdrawal from the 2015 nuclear agreements, the Iranian Parliament passed a law allowing the government to begin 20% uranium enrichment during 2021, which contravenes the terms of the U.N. agreement.

On the other hand, the confrontation between Iran and the Gulf monarchies, Saudi Arabia and the UAE, is being expressed with greater violence in Yemen and Syria and the permanent tension in Iraq and Lebanon.

- Non-OPEC Production

As for the nine non-OPEC countries that agreed to reduce their production (Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Oman, Russia, Sudan, and Southern Sudan), in December 2020, they recorded production of 12.76 MMBD, 14.7% of world production.

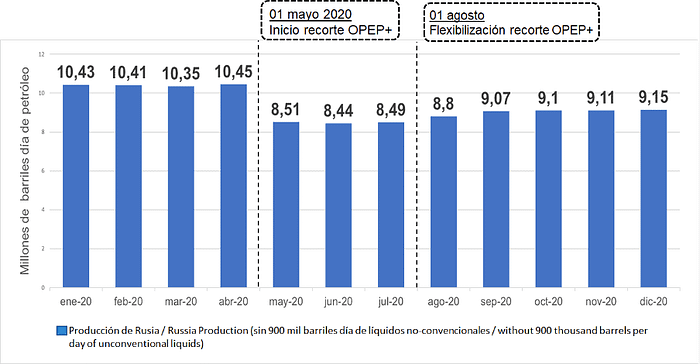

Russia had a production of 9.15 MMBD of oil, 40 thousand barrels a day more than last November, not complying with the assigned quota for the sixth consecutive month, with an overproduction of 157 thousand barrels a day of oil. Since July 2020, Russia has presented an overproduction of more than 100 thousand oil barrels per day.

RUSSIA’S PRODUCTION IN 2020

(January-December)

Source: Own elaboration with production data of the Ministry of Energy of Russia and non-conventional liquids registered by OPEC.

OPEC+ production cut

In December, OPEC+ countries cut 7,648 MMBD, meeting the agreed cut quota of 7,682 MMBD by 99.56%. OPEC-10 cut 4,978 MMBD, meeting 102.26% of its quota of 4,868 MMBD, representing 65% of the group’s production cut.

This compliance is primarily due to the production off-sets from Angola and Nigeria, which cut an additional 82,000 and 75,000 barrels a day, respectively, to their cut quota.

However, the behavior of small producers stands out, such as Gabon and Equatorial Guinea. They exceeded their production quota by 27 thousand and 23 thousand barrels a day, respectively, failing to comply with more than 80% of their production cut agreement. Iraq presented an over-supply of 44 thousand barrels a day of oil.

For their part, the nine non-OPEC countries recorded a production cut of 2,670 MMBD, 94.9% of their quota of 2,814 MMBD, which represents 35% of the OPEC+ cut.

However, despite being one of the group leaders, Russia has not fulfilled its agreed quota in the last six months of 2020, registering a production surplus that exceeds 100 thousand oil barrels per day. At the same time, they will be one of the countries that will increase their production quota in February and March.

U.S. oil production

U.S. production during December 2020 and up to the week of January 8th was 11 MMBD, according to the weekly EIA report of January 13th, 2021, the same level of production as nine weeks ago. This balance is expected to be maintained in 2021, while the new U.S. President develops an energy policy. Joe Biden signed 15 executive orders immediately upon being sworn-in as president, including the revocation of the permit to the Keystone XL pipeline, which has been much questioned due to its environmental implications.

For this year, EIA estimates that the U.S. will maintain the production levels of November and December 2020, with an average of 11.1 MMBD, 200 thousand barrels of oil per day less than the average of 2020. By 2022, production will average 11.5 MMBD.

The American Shale oil

Shale oil producers have had a year of significant impact on their production capacities due to the collapse of prices below $45 per barrel starting in the first quarter of the year. The above made it practically impossible to continue production and fracking operations and drilling new wells, given the production costs.

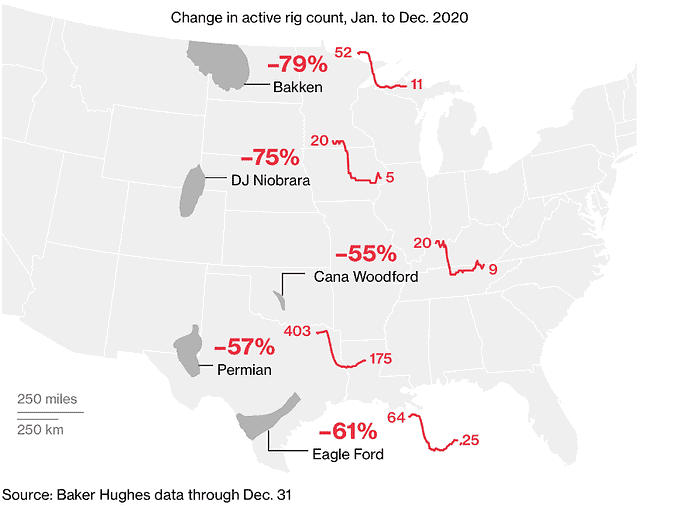

IMPACT ON PRODUCTION ACTIVITY IN NORTH AMERICAN SHALE OIL AREAS 2020

Source: Bloomberg, Baker Hughes

This effect on shale oil producers was reflected in U.S. production decreasing from its historical levels of 13 million barrels of oil per day between January and March 2020 to the current levels of 11 million barrels of oil per day. A fall of 15% in 10 months directly correlates with the collapse of oil prices.

CORRELATION BETWEEN OIL PRICES AND SHALE OIL

Source: Baker Hughes, Bloomberg

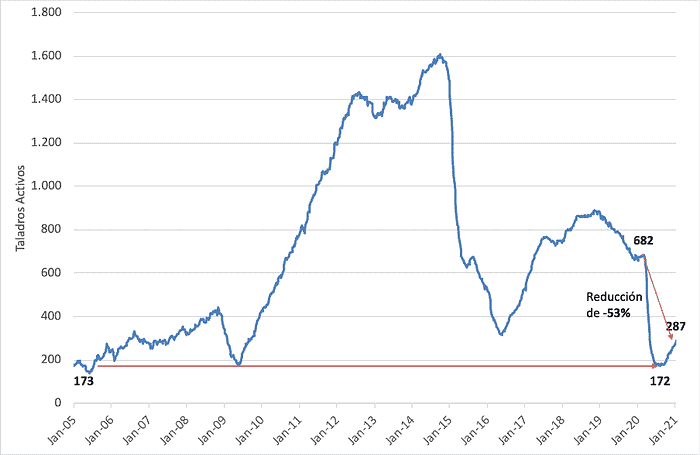

The decrease in shale oil has been reflected in the collapse of active drills in the country. This indicator has fallen from its maximum 682 active drills on March 2nd, 2020, to the lowest levels registered on August 14th, 2020, with 172 active drills, similar to levels in 2005.

As of August, with a $40.65 per barrel price, drilling activity has recovered to reach 275 active drills as of January 8th, 2021. These levels are similar to those of 2010, at the beginning of the shale oil boom.

DRILLING ACTIVITY IN THE U.S.

(2005–2021)

Source: Baker Hughes

The OPEC+ production cuts in force since May have been recovering oil prices to levels that have allowed shale oil producers to restart activity, the OPEC+ production cuts in force. The decision to cut additional production from Saudi Arabia underpins a price level above $50 per barrel, which is beginning to be a floor of viability for shale oil producers.

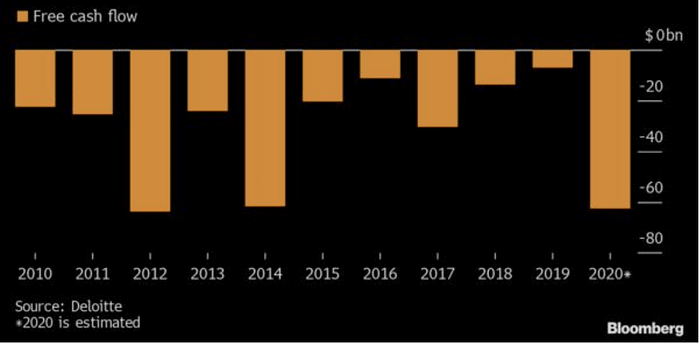

This sector, with higher production costs than the rest, composed mostly of independent, small, and medium-sized companies, has been significantly affected by the financial burden of its operations since most of them have incurred large debts in a business that is financed by hedge funds, a sector that since 2010 has required more than 342 billion dollars for its operations.

SHALE OIL CASH FLOW

(2010–2020)

Source: Bloomberg

Since the beginning of the market crisis in 2020, the Shale Oil sector has been burdened by debts to banks of more than 200 billion dollars.

For this reason, in May 2020, Trump’s administration committed to keeping the sector afloat, requesting a $2.2 billion financial support package to Congress, called the CARES act. Thirty-seven oil companies claimed a total of $1.9 billion as part of the massive tax breaks in the middle of last year, which was rejected by Democrats in Congress.

As a result, more than 250 Shale Oil companies have filed for Chapter 11 Bankruptcy this year. There has been a process of acquisitions and mergers, from which the large North American oil companies, such as Exxon Mobil, Chevron, and ConocoPhillips, have benefited, positioning themselves as important producers of Shale Oil.

For this reason, the remaining small and medium-sized Shale Oil companies, with no financial support, seem more oriented at the beginning of the year to use the resources coming from price-increase to pay off debts and pay dividends instead of drilling new wells. For this reason, the EIA and the IEA estimate that oil production in the U.S. will remain at current levels throughout this year. This maneuver is the producers’ response to their financial and dividend sharing commitments amid an environment of expectation for the sector in the face of the new Democratic administration’s policies and their zero-net-emission energy policy for 2050.

ECONOMY

World Bank: Prospects for 2021

According to the World Bank’s estimates in its January 2021 World Economic Outlook, the world economy is expected to shrink by 4.3% in 2020 and grow by 4% in 2021, assuming that vaccines for COVID-19 will be global in scope throughout the year. During 2020, since its escalation in the first quarter of last year, the pandemic has caused more than two million deaths and depressed productive activity in the economies of the U.S., U.K., Europe, and Asia.

Short-term country priorities include controlling the spread of COVID-19 and ensuring rapid and widespread deployment of the vaccine. The latter is the most complex to achieve because developing countries are lagging in accessing available doses. In this context, where the high levels of contagion are maintained, there would be a lower growth scenario than the one initially estimated, which would be around 1.6%, according to the World Bank.

In the case of the most industrialized countries, the expected growth would be around 3.5%, always below the proportion of their 2020 declines, after the sharp rebounds of the pandemic (the United States -3.6%; European Union 7.4%; Japan -5.3%), while emerging and developing economies are expected to grow by 5% in 2021 (with China reaching 7.9%), after a contraction of 2.6%. For low-income economies, activity is expected to increase by 3.3% in 2021, after a contraction of 0.9% in 2020.

The main threat to economic recovery in emerging markets and other developing countries, besides the lack of access to vaccines, is the accumulation of external debt, which has increased as a proportion of countries’ GDP and could slow down long-term growth and lead to a global debt crisis.

EXTERNAL DEBT AS A PERCENTAGE OF GDP

Source: World Economic Outlook, World Bank, January 2021.

Finally, the World Bank concludes that, due to the pandemic, world economic growth will be more limited in the long term. The above, due to lack of investment, underemployment, and workforce’s decline in some of the advanced economies, as is already happening in the United States or the European Union.

United States: New Administration.

On Wednesday, January 20th, Joseph (Joe) R. Biden was sworn-in as the 46th president of the United States, replacing Donald Trump. The inauguration was secured by more than 25,000 National Guards, without spectators, and amidst strict security measures, after the unprecedented events of January 6th, when pro-Donald Trump protesters stormed the Capitol, ignoring the results of the last election and trying to prevent the confirmation of the results by Congress that same day.

Biden assumes the presidency, amid the country’s profound division, with the notable absence of outgoing President D. Trump, who was subjected to an impeachment process for the second time in his mandate, accused by the Democratic majority and the head of the Republican party of having instigated the assault on the Capitol.

In an anxious country, affected by a severe economic crisis, unemployment, and the health emergency of the Covid-19, as soon as he was sworn in, President Biden signed more than 17 executive orders, repealing decisions of his predecessor. Among them was the revocation of the permit for constructing the border fence with Mexico, the license for the Keystone XL oil pipeline project in Canada, and a moratorium on Alaska’s oil and gas activities that the outgoing administration had opened for development.

These measures are in line with the goal announced in previous weeks of “zero net emissions by 2050,” to mitigate global warming impacts, using restrictions on fossil fuels, and promote massive investments in alternative energies.

On migration policy, Biden proposed legislation to allow the estimated 11 million undocumented immigrants to become citizens within eight years.

The project proposes to grant temporary legal status during the first five years and then eligibility for a residence permit (Green Card), after paying taxes and background checks, among other measures. After three years, they can apply for citizenship.

The legislation will also restore and expand programs for refugees and asylum seekers and allocate new funding for foreign aid to Central American countries, increased opportunities for foreigners to work in the United States, and improved border security.

Financial Aid Package

On Tuesday, Janet Yellen, Biden’s nominee for Secretary of the Treasury, advocated lawmakers for a tax relief package proposed this week to aid the nation’s economic recovery.

A $1.9 billion rescue package was announced on Thursday, January 14th, by President-elect Joe Biden to combat the COVID-19 pandemic and help the economy. Of the total, $400 billion would go directly to fighting the pandemic, while $350 billion would be given to state and local governments to overcome budget shortfalls. This proposal provides for checks of $1,400 per person, within annual income limits, completing the $600 checks for the aid package that was approved last December.

Amid the political turbulence related to Trump’s departure from the White House and his second impeachment, which Congress approved, the U.S. nation continues to face serious economic problems, with 6.7% unemployment registered last December, according to the U.S. Bureau of Labor Statistics.

In the week of January 4th alone, 1.15 million people applied for unemployment benefits (a 25% increase over the previous week). Also, self-employed and part-time workers filed another 284,000 applications for emergency federal support.

Biden’s proposal also provides emergency paid leave for 106 million Americans, regardless of their employer’s size. It also includes tax credits for families to off-set up to $8,000 a year in child care expenses.

The president-elect also proposes to extend unemployment benefits until the end of September this year and will ask Congress to raise the federal minimum wage to $15 an hour.

After Biden’s announcement last week, the U.S. markets did not react positively to this plan. However, after Yellen’s express support, the leading Wall Street indices rose on Wednesday, January 20th, suggesting confidence in the new administration’s measures.

Economic Outlook for Asia

Economic analysts expect Asian markets to be the fastest to begin their economic recovery from the COVID-19 pandemic, with the People’s Republic of China continuing to lead the regional push through 2021.

As already mentioned, China was the only country in the world that increased its GDP in 2020.

The recent agreement to establish the Comprehensive Regional Economic Partnership,50 the free trade agreement between the 15 states of Asia and Oceania, which involves more than 2.2 billion people and 32% of global GDP, will be decisive in the new regional trade relations, even before its ratification.

On the other hand, according to analysts from the London firm GlobalData,51 India is expected to grow by 9.7% during 2021, becoming the fastest growing economy in the world, above China, which is estimated to have a GDP growth of 8.6%.

The above is based on estimates of massive inflows of foreign direct investment into the country in recent months, the Narendra Modi government’s economic stimulus package of more than 20 trillion rupees ($266 billion), the expected growth in industrial activity, the recent fall in the COVID-19 cases in India and the revitalization of domestic demand.

European Union:

On the same day that the new U.S. administration took office, the European Commission president, Ursula von der Leyen, celebrated Joe Biden’s arrival at the White House, while expressing her optimism about relations between the United States and the European Union.

It is worth remembering that the United States and the European Union were confronted on several issues after Trump’s arrival in January 2017: from international trade and the re-imposition of tariffs to climate change, international policy positions were contrary to multilateralism, which altered the usual coordination between the two actors.

Last December, the European Union announced a plan to improve the transatlantic relationship. It consists of four major policy areas: health response to the pandemic, climate change, trade and technology, and security.

The ECB and Bitcoin

The President of the European Central Bank, Christine Lagarde, issued a statement last Wednesday 13, asking for global regulation for the Bitcoin cryptocurrency. She affirmed that “the digital currency had been used for money laundering activities in some cases and that it was necessary to close any loopholes,” given the often anonymous nature of those acquiring this asset.

Lagarde did not provide specific examples of money laundering cases but said he understood that there had been criminal investigations into illegal activities. The crypto sector is not regulated beyond existing global anti-money laundering standards.

Bitcoin and other digital currencies are acquired by investment funds, large corporations, and also individuals. Among its characteristics, it stands out in its independence from governments, banks, and global corporations. Since last March, its value has increased almost tenfold, reaching its maximum historical value of $42,000 per unit in January 2021.

BITCOIN

(October 2020 — January 2021)

Source: Bitcoin Quote (capital.com)

The increment of more than 300% in one year is mostly explained by the entry of large investors who see Bitcoin as an alternative form of reserve money value, comparable to gold. The firm J.P. Morgan affirmed that, in the long term, it could reach 146,000 dollars. Other players are more skeptical and claim that Bitcoin is just a speculative bubble.

Post-Brexit: the British economy in trouble

The new commercial relationship between the United Kingdom and the European Union,54 its largest trading partner, began on January 1st, 2021, with the first setbacks experienced by the British side, particularly concerning the logistical aspects of exports, complicating the arrival of products from the United Kingdom to the countries of the Union.

Under the new agreement, European companies’ shares could no longer be traded on the London-based financial platforms where they had historically been traded. They migrated to other exchange points, such as Amsterdam or Paris.

This week, Andrew Bailey, the governor of the Bank of England, the U.K.’s central bank, told a parliamentary committee that the Brexit deal would cost the British economy about 2 percent of gross domestic product the next few years. The Bank of England’s Governor, Andrew Bailey, has been a critical figure in the U.K.’s economic recovery. The same would be caused by additional bureaucracy for customs declarations and other commercial expenses.

The food for export produced in Great Britain to the European Union is the most affected commercial goods. The leading cause of these delays is not having the documentation required by European countries, putting at risk products that are subject to spoilage and must have precise delivery times, such as fishing products.

Thus, for many British companies, Brexit resulted in logistical, regulatory, and administrative problems. There was insufficient preparation due to the trade agreement’s late date (only on December 24th).

In the current context, with the pandemic at its worst and companies dedicated to survival, amid a national blockade, some analysts say that the economy could be heading for a double-dip recession. In other words, when a second recession begins before the recovery from the first recession, which started last year, is complete.

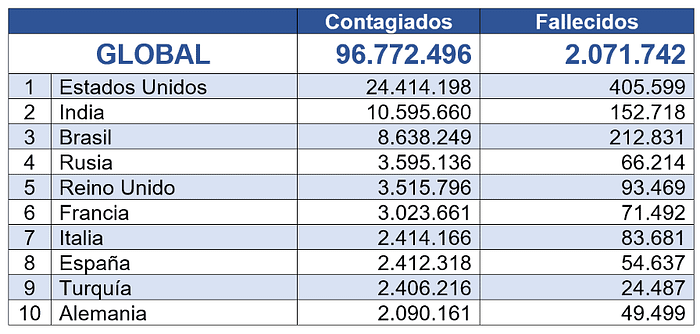

COVID-19

The pandemic has infected nearly 97 million people and killed more than 2 million worldwide, while 53 million people have recovered from the virus. The numbers as of January 20th, 2021, are as follows:

COUNTRY RANKING OF CONTAGIONS AND DEATHS — COVID-19 (January 2021)

Source: Interactive map of the Johns Hopkins University Center for Science and Systems Engineering https://coronavirus.jhu.edu/map.html. Classification according to the number of infections.

In the United States, the country with the highest number of COVID-19 infections and deaths, President-elect Joe Biden signed executive orders mandating the use of masks in all federal buildings in the country, placing the fight against the pandemic as one of his government’s priorities. He also appointed David Kessler to lead Operation Warp Speed, the program to accelerate the development of vaccines for COVID-19. Kessler helped accelerate AIDS drug development and approval in the 1990s as head of the Food and Drug Administration (FDA).

The Asian region has been shaken by the worst COVID outbreak in China since last summer, with more than 28 million people quarantined. The closure includes the cities of Shijiazhuang, Xingtai, and Langfang and the districts of Beijing. Beijing’s concern that the outbreak could get out of control and threaten its economic recovery. While India has the second-highest number of infections worldwide, and Japan extended its state of emergency due to increased infections and its overburdening health system. The cancellation of the Olympic Games, which were canceled last year to be held in 2020, is taken for granted.

Europe, which totals 30 million cases and more than 662,000 deaths, most countries have imposed severe restrictions, particularly in Germany, Italy, Spain, and France, the member countries most affected. For his part, the top official of the World Health Organization in the region reported that 25 of the 53 European nations had detected infections with new variants of the virus, calling for stricter public health controls to slow its transmission.

In Brazil, the third country with the most cases globally and the second with the highest number of deaths, scientific authorities and organizations have had to face countless problems in dealing with the pandemic. The most serious of these has been President Jair Bolsonaro’s open opposition to taking more effective measures to contain the pandemic, as well as the massive supply of vaccines.

The South American giant has also authorized the emergency application of vaccines from Sinovac Biotech (China) and AstraZeneca (U.K.). The above, despite the recent controversy due to the opinion of Brazilian scientists, who affirmed that the Chinese vaccine CoronaVac, had an effectiveness of only 50.4% and not the 78% that was affirmed by the pharmaceutical company.

If this figure is accurate, it could condition Brazil’s immunization process, a country that has already ordered 65 million doses from Sinovac Biotech. The president of the Chinese pharmaceutical company, Yin Weidong, rejected these statements, confirming that the phase III clinical trials carried out on CoronaVac, “are sufficient to demonstrate its safety and efficacy.”

Complications with the vaccine

The progress made by the deployment of recently approved coronavirus vaccines has improved the economic outlook for 2020. However, the shortage and logistical difficulties in supplying the vaccines prevent the normalization of global economic activity, meaning that the pandemic cannot be solved during the current year, extending into 2022.

In a context where the distribution of vaccines at a global level is still limited, new variants of the coronavirus have been discovered in more than 50 countries, further complicating the picture. Europe is already experiencing the consequences of the third wave of the pandemic, while the United States continues to break negative records in terms of the emergency itself.

With the developed countries monopolizing the available doses, the arrival of the cure against COVID-19 looks complicated for the developing world. In contrast, countries with large populations, like India and Brazil, which occupy the second and third position in the world in the number of infections and the third and second in deaths, may worsen their situation.

These countries may have the resources to purchase vaccines from manufacturers (Brazil) or produce them domestically (India). Regarding the Asian country, on January 16th, it began a massive vaccination campaign that aims to apply 300,000 doses per day until 300 million of its 1.3 billion inhabitants are vaccinated by August 2021. Brazil had already begun to apply the Chinese CoronaVac vaccine, among others, but amid severe limitations due to its health system’s collapse.

Unfortunately, this is not the situation for other countries in Latin America or Africa, which lag in the bidding for limited doses.

On Tuesday 19, during a meeting of the World Health Organization’s Executive Board, its Director-General, Tedros Adhanom Ghebreyesus, criticized the fact that high-income countries are taking advantage of the developing world to procure vaccines against COVID-19.

As an example, Ghebreyesus noted that so far, more than 39 million doses of vaccine have been administered in at least 49 higher-income countries and mentioned that only 25 doses had been administered in one lower-income country.

He also expressed his concern that bilateral agreements signed by high-income countries monopolize the available doses of vaccines, threatening the installation of COVAX. This mechanism seeks to accelerate the development, production, and equitable access to tests, treatments, and vaccines of COVID-19. In this way, the conditions that the mechanism seeks to avoid are produced.

Therefore, it expressly requested developed countries prioritise COVAX since this mechanism will also allow access to doses for health workers and older populations in low-income countries.

DEMAND

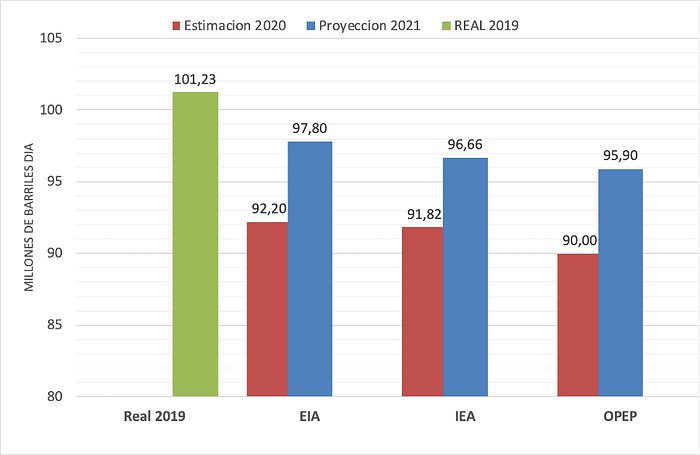

Oil consumption in 2020 is revised downward from what was projected in November by various organizations.

For the EIA, in its Short-Term Perspective (STEO) report published on January 12th, consumption for the year was 92.2 million barrels per day, 9% below demand in 2019.

On the other hand, in its monthly market monitoring report (MOMR), of January 14th, OPEC showed world consumption at 90 million barrels a day in 2020. A 9.8% drop in demand concerning the previous year, with a reduction in demand by 11.6% in OECD countries, with an average of 42.16 million barrels a day, since real consumption in the second quarter was weaker than expected.

Regarding consumption in 2021, no total recovery in demand is expected. OPEC maintains its forecast for 90 million barrels per day, an increase of 7% over consumption in 2020.

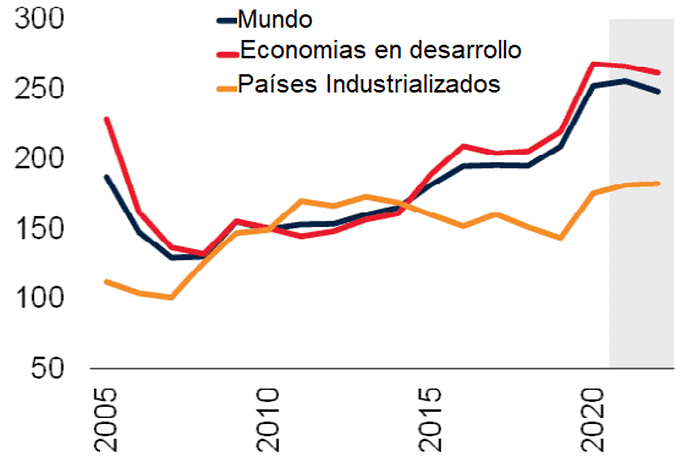

ANNUAL VARIATION OF DEMAND WORLDWIDE

(2019–2021)

Source: Own elaboration, Data from the Energy Information Administration and the International Energy Agency, OPEC, January 2021.

On the other hand, the EIA lowers its projections for the previous month and places 2021’s demand at 97.8 million barrels per day. A more optimistic projection than OPEC’s, with a recovery of 5.6 million barrels per day.

In the International Energy Agency’s (IEA) report, published on January 20th, they slightly lowered their estimates of demand for 2021, with a recovery of 5.5 million barrels per day, similar to EIA forecasts. According to the IEA, the recovery in demand will be boosted in the second quarter, when the results of the vaccinations and the economic reactivation will be seen.

This upward trend would have its most significant upturn in the second quarter of 2021, led by Asia — mainly China and India — and will continue in 2022 when demand is expected to increase to 101.08 million barrels per day. Therefore, although consumption will increase in 2021 and 2022, it will still be between 2% and 4% below demand in 2019.

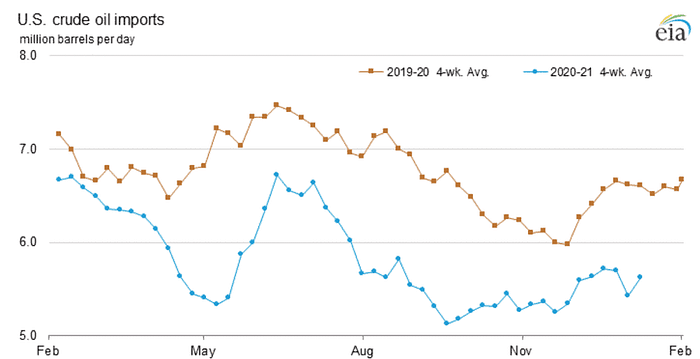

USA

According to data published as of January 8th, oil imports increased to 6,239 million barrels per day, representing 16% concerning the previous week, when they registered four consecutive weeks of decline.

U.S. OIL IMPORTS

(2019–2021)

Source: Energy Information Management

STORAGE

According to preliminary data from the EIA’s STEO report, at the end of 2020, inventories of crude oil and other liquids in OECD countries averaged 3,051 million barrels as of January 12th, 5.81% above the average recorded in 2019.

At the end of 2020, inventory drainage increased due to a surge in oil demand in Asia, in addition to strict compliance with OPEC+ production cuts. EIA estimates predict that world oil inventories will continue to decline, specifically by 0.6 million barrels per day in 2021 and by 0.5 million b/d in 2022.

The EIA estimates, in its weekly report This Week in Petroleum, published on January 13th, that the most extensive extraction of inventories will take place during the first quarter of 2021 and will be 2.3 million barrels per day.

The increase in production in Libya, Russia, and Kazakhstan could slow down the reduction of inventories. However, this increase in supply will be compensated by reducing one million barrels a day of oil from Saudi Arabia for February and March.

USA

According to preliminary EIA data, in 2020, storage had a historical rebound, reaching 1,344 million barrels, 1.74% higher than the average for the first quarter of that year. It is estimated that the trend will be downwards in 2021 and 2022, to 2,951 and 2,919 million barrels, respectively.

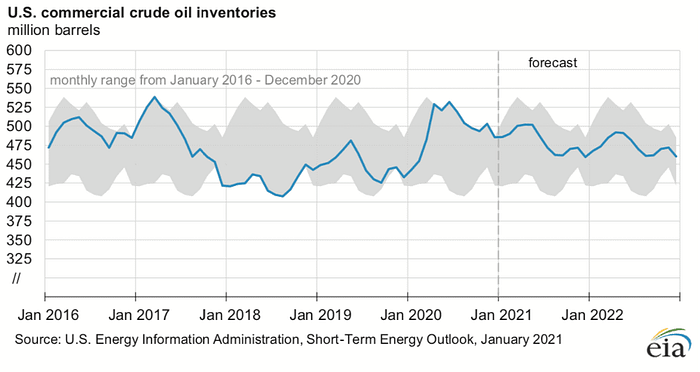

U.S. commercial inventories continue to fall since five weeks ago, reaching 482,211 million barrels, according to the report This Week in Petroleum published on January 13th, which reflects a reduction of 11% to the historical levels registered in June 2020, directly favoring the recovery of oil prices.

U.S. CRUDE OIL STORAGE

(2016–2022)

Source: Energy Information Management

Last December, the strategic reserves remained unchanged. On January 13th, they stood at 638,085 million barrels, which, despite a notable reduction, are still 0.63% above the levels recorded in January 2020.

The rebound in the storage of U.S. strategic reserves took place during the second quarter as a strategy to take advantage of the historical fall in prices. They were currently drained 3% to July due to the meteorological events in the Gulf of Mexico that stopped production in several opportunities during the third quarter, which forced the use of these reserves for the operating refineries’ diet.

As for coverage days, as of December 13th, they stood at 33.6 days, and although they register eight weeks of consecutive decline, they are still 23% above the 2019 average.

VENEZUELA

The year begins with gloomy prospects for the country. The severe economic crisis is deepening with a massive deterioration in Venezuelans’ quality of life, whose monthly minimum wage (1 dollar, 0.03 cents per day) is one of the lowest globally, far below the United Nations poverty line of $1.90 per day. In the context of a dollarized economy, that the government claims as “a blessing,” while 96% of the population is in poverty.

The country’s hyperinflationary process has been suffering for at least five years, stimulated by the government’s massive emissions of inorganic money, placed the official exchange rate at 1,561,382.13 bolivars per dollar, which has made the bolivar disappear de facto as legal tender in the country. While more than 70% of operations are transacted in dollars, the government uses the bolivar to pay wages and salaries, placing the Venezuelan labor force among the cheapest in the whole world.

For its part, the Venezuelan economy has suffered a severe contraction since 2015, with an accumulated drop in GDP of 72%, which has not only dismantled the national productive apparatus, including the oil sector but has caused millions of Venezuelans to be without quality jobs, underemployed and underpaid. Together with the lack of supplies and services, the political crisis has caused a massive exodus of Venezuelans. According to the UNCTAD, for November 2020, it already reaches the figure of 5.4 million Venezuelans who have left the country.63

Amid this unprecedented crisis, the government of Maduro continues to control all the political spaces in the country, voting for a new National Assembly, which is not internationally recognized as it is the result of an electoral process marred by irregularities. In contrast, it continues to increase repression, censorship, and imprisonment against the country’s political, social and working sectors.

Oil Production

The oil sector does not escape this situation of deep crisis and dysfunctionality of the Venezuelan State; on the contrary, it is the center of the economic crisis and the sector most affected by the mismanagement and the new oil policy of the government.

Last February 2020, the government decreed one more intervention of the oil industry and PDVSA, after an internal process of repression and imprisonment of managers that resulted in the company’s militarisation in December 2017 and the collapse of oil, fuel, and gas production in the country.

The intervening Commission arrived at the company with a privatization plan that has been put into effect, but that, far from increasing oil production, as the government had promised, has deepened the operational and management problems of PDVSA, whose production has fallen 2.6 million barrels of oil per day between 2014–2020.

The Intervention Commission received a production, already reduced, of only 760 thousand barrels of oil per day in February 2020 and last December closed with a production of 431 MBD, a fall of 43.3% in 10 months, in addition to the collapse of the national refinery system, which operates at only 10% of its capacity.

OPEC’s monthly report for January, corresponding to December data, reflects, according to information from secondary sources, that crude oil production reached barely 431 thousand barrels per day.

PRODUCTION OPEC COUNTRIES (2018-December 2020)

Source: OPEC’s MOMR

As we have warned in previous Bulletins, the government’s mismanagement in PDVSA, along with the militarization of managerial positions, the harassment of workers and the diversion of resources from operations, investment, and maintenance of the company, to the payment of government commitments between 2015–2017, caused the operational collapse of the company, one of which was 96% of the nation’s income.

This drop in its oil production places Venezuela as OPEC’s 10th oil-producing country, dropping seven seats in just seven years, only above small producers who have not been in the organization for more than three years.

At present, PDVSA cannot sustain reliable, stable, and secure operations because all its operational, administrative, and control processes have been violated.

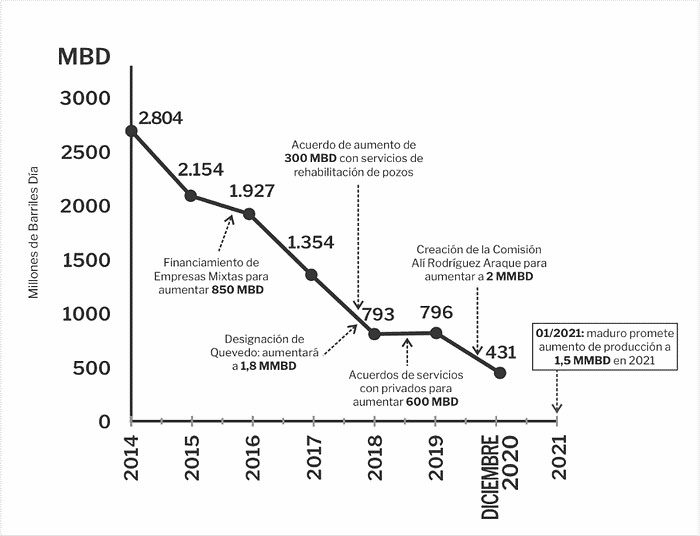

Although oil production has only declined between 2014–2020, in the government’s annual message, Maduro assures that it will increase production in 2021 from current levels to 1.5 MMBD, which seems unlikely, given the company’s dismantling and the delay in investments.

VENEZUELAN OIL PRODUCTION (2014 — Dec 2020)

Source: MOMR OPEP data, own elaboration

It is not the first time that Maduro’s government announced increases in the country’s decimated oil production, a situation that has occurred precisely because of its successive interventions in the company and its dismantling, which is part of a deliberate government policy to weaken the company for privatization.

Thus, in November 2016, when he announced joint-ventures financing for 10.7 billion dollars, he promised an increase in production of 850 MBD.

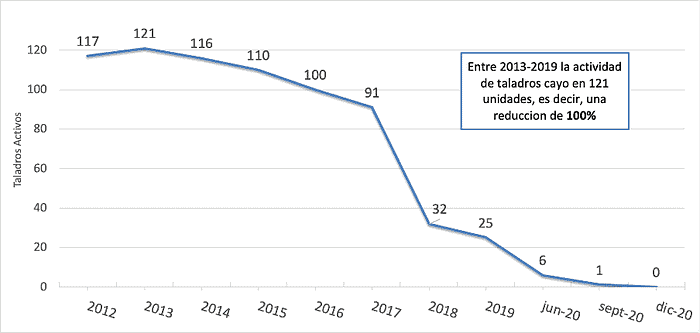

In September 2017, an agreement was signed with the companies Schlumberger and Halliburton to rehabilitate 800 wells in the north of Monagas and Zulia states to increase 300 MBD of production. Still, the reality is that between 2017 and 2018, drills’ activity fell by 65%, and at the end of 2020, according to the OPEC report, there are no active drills in Venezuela, nor the corresponding oil production.

ACTIVE DRILLS IN VENEZUELA

(2012–2020)

Source: MOMR OPEP data, own elaboration

With General Manuel Quevedo’s appointment in November 2017, Maduro promised to increase the country’s oil production by 1.8 million barrels a day in one year, but, on the contrary, what happened was that production fell 41% to 2017. The most significant year-on-year decline in the industry. In parallel, the industry is being militarized, and persecution of the company’s managers and directors has been unleashed, which has resulted in more than 100 workers imprisoned and the departure of more than 30 thousand workers, engineers, and qualified personnel from PDVSA.

In August 2018, within the framework of Decree 3,368, and in violation of the provisions of the Organic Law on Hydrocarbons, 14 joint service agreements were signed with private parties, within the framework of the Integral Project for Production Recovery, with service providers such as Well Services Cavallino C.A.; Petrokariña C.A.; Helios Petroleum Services C.A.; Shandong Kerui Group; Consorcio Rinoca Centauro Karina; Consorcio Petrolero Tomoporo and Venenca, to increase oil production by 660 MBD. This was denominated by General Quevedo, still president of the company, as the “beginning of a new era within PDVSA,” thus showing the industry’s direction with the delivery of its operations to private parties. This policy is now strengthened with the new Intervention Commission and the approval in the extinct National Constituent Assembly of the unconstitutional law called Anti-Blockade Law.

The company has followed the government’s policy of no transparency. PDVSA lacks audited financial reports and has no compliance to the State control agencies, in a re-edition of PDVSA’s “black box” during the Oil Opening of the 80s and 90s.

Venezuela loses CITGO

This week, a judge in Delaware authorized the sale of shares of CITGO, a US-based subsidiary of PDVSA, to pay the $1.4 billion that Maduro’s government committed in November 2018 to the Canadian mining company Crystallex. The above completes an initial payment of $425 million for its liquidation of assets in the country, an excessive amount considering that the Canadian company did not make any type of investment or gold extraction in the country.

With this decision, the Venezuelan government continues to lose control of its assets abroad due to inadequate legal and asset management abroad.

The anti-blockade law and illegal conditions to attract investors

The Reuters news agency assured, last January 14th, that Nicolás Maduro’s government, through PDVSA, offers to minor businessmen in the country new conditions to stimulate investment in some oil fields.

These conversations are taking place at a time when the Venezuelan oil industry is facing the most profound crisis in its history, in addition to U.S. sanctions, which, although not the source of PDVSA’s collapse, have restricted the levels of Venezuelan oil exports.

To date, it is unknown whether these companies have formalized their participation in these agreements; however, delays in payment commitments to PDVSA contractors and U.S. sanctions for those who provide services to the Venezuelan State are a limitation the time of establishing any negotiation.

Although the government has stated the purpose of privatizing PDVSA and handing over the oil to foreign operators, it has not successfully attracted international companies. This is, fundamentally, because the international oil sector, including Russian and Chinese companies, is reluctant to establish new agreements with the government, both because of its legitimacy problems and the violation of constitutional reserves and the legal framework hydrocarbons.

Based on the experience of the country’s oil operators, they know that any investment or development in the sector based on the Anti-Blockade Law and in violation of the legal framework for hydrocarbons in the country carries significant risks for their investments when the internal political situation and the government change.

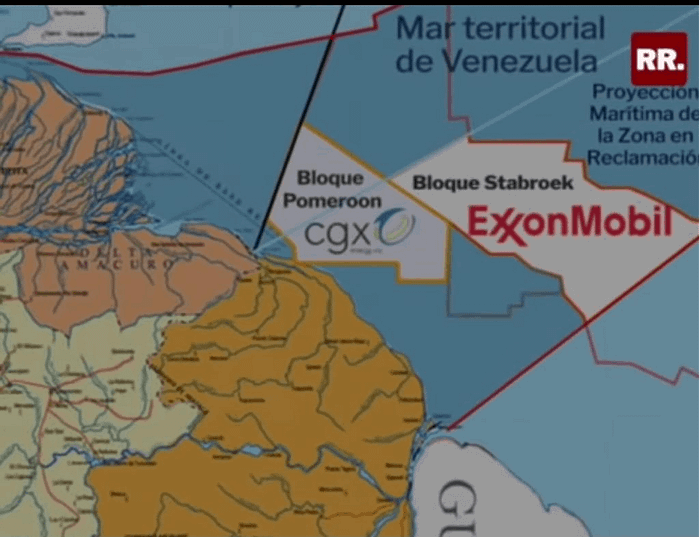

Essequibo Negligence

The inaction and negligence of the Maduro government in handling the controversy with Guyana over the Essequibo territory has allowed Exxon Mobil and other North American and Chinese transnationals to start exploiting the vast oil resources located in the territorial sea of the territory and on the Atlantic coast of Venezuela.

TRANSNATIONAL PRESENCE IN ESSEQUIBO

Source: Own elaboration. www.rafaelramirez.net

In January 2020, the first export of crude oil produced in that territory was made: one million barrels headed to Exxon’s refineries in the Gulf of Mexico, a cargo with the quota of crude to which the North American company has the right of ownership, according to the Guyana-ExxonMobil agreement. In February of the same year, Guyana made its first export with the quota of crude to which it is entitled — according to the same agreement — also of one million barrels of oil and the same destination.

In October 2020, Guyana’s oil production reached 105 thousand barrels per day of crude oil in the Liza field of the Stabroek block (on the coast of the Essequibo and the Venezuelan Atlantic Platform). According to ExxonMobil’s discoveries, it is estimated that it could reach 350 thousand barrels per day in 2021 and 750 thousand barrels of crude oil in 2025.

Currently, the companies Esso Exploration and Production Guyana Ltd., a subsidiary of ExxonMobil (the operator of the block); Hess Guyana Exploration Limited, a subsidiary of the American Hess Corporation; and CNOOC Nexen Petroleum Guyana Limited, a subsidiary of CNOOC International, are the companies that operate in the Stabroek block.

It is estimated that the recoverable reserves in this block are in the order of 9 billion barrels, including oil and gas, plus another billion barrels (not yet quantified) of potential exploration.

Production activities in Guyana continue. On September 30th, 2020, ExxonMobil announced that it will continue with the development of Stabroek, this time in the Payara field, which has a gross production capacity of 220 thousand barrels/day and whose production will start in 2024.

The North American company ExxonMobil acts illegally concerning the exploitation of resources in the referred area because they are “unauthorized” operations in the territory in dispute between Guyana and Venezuela, even though the Guyanese government has unilaterally approved them.

This oil production is subject to legal questioning since the hydrocarbons produced are part of the territorial dispute between Guyana and Venezuela, representing the plundering of natural resources and a violation of Venezuela’s national sovereignty.

All of this happens in the face of inaction and disconcert of Maduro’s government, which has been negligent in handling the dispute with Guyana. The situation of the territorial dispute has been discussed before the International Court of Justice, after the U.N. Secretary-General, Antonio Guterres, desisted from acting as the Good Officiant, as established in the Geneva Agreement of 1966. This decision has meant a diplomatic victory for the Guyanese government and a resounding failure for Venezuela.

Today Exxon Mobil and other transnational oil companies, taking advantage of the profound weakness of the Venezuelan government and the ambitions of the political sectors of Guyana, have opted to develop the oil resources of the Essequibo territory in a reckless act of dubious legality, which makes the area an eventual conflict zone in the near future.

BIBLIOGRAPHIC REFERENCES:

- The 12th OPEC and non-OPEC Ministerial Meeting concludes, OPEP, 03 diciembre 2020.

- Saudi Arabia to Cut Oil Production Sharply in Bid to Lift Prices, Wall Street Journal, 05 enero 2021.

- Weekly Stocks, Administración de Investigación Energética de EE.UU., 06 enero 2021.

- Las mutaciones del coronavirus hacen más difícil la lucha contra la pandemia de COVID-19, advierte la OMS, Organización de las Naciones Unidas, 11 enero 2021.

- China urges people to avoid holiday travel as COVID cases jump, Al Jazeera, 15 enero 20121.

- OPEC daily basket price stood at $55.75 a barrel Wednesday, 20 January 2021. OPEP, 21 enero 2021.

- 13th OPEC and non-OPEC Ministerial Meeting concludes, OPEP, 05 enero 2021.

- Saudi Arabia surprises market with 1 million b/d ‘preemptive’ output cut, S&P Global Plats., 05 enero 2020.

- Saudi Arabia raises February crude official prices to Asia, Reuters, 06 enero 2021.

- Saudis pledge to cut oil output despite Russian increases, Financial Times, 05 enero 2021.

- Russia’s OPEC+ position to increase output requested by oil companies, Tass,m 05 enero 2020.

- 2021Arabia Saudí elimina el bloqueo a Qatar. Atalayar, 05 enero 2020.

- The UAE Warns U.S. Shale Companies Against Pumping More Oil, Bloomberg, 12 enero 2020.

- Saudi Oil Min. Says Cut Is Commercial Choice, Not Political, Bloomberg TV, 06 enero 2021.

- Monthly Oil Market Report, OPEP, 14 enero 2021.

- Statistics, Ministerio de Energía de Rusia, enero 2021.

- Short-Term Energy Outlook, Administración de Info0rmación Energética de EE.UU., 12 enero 2021.

- Oil Market Report — January 2021, Agencia Internacional de Energía, 19 enero 2021.

- The 10th (Extraordinary) OPEC and non-OPEC Ministerial Meeting concludes, OPEP, 12 abril 2020.

- Iraq increases capacity of Baiji refinery to 140,000 bpd, ministry, Xinhuanet, 11 enero 2021.

- ISIS attacks Iraq’s Baiji oil refinery, Deutsche Welle, 18 junio 2014.

- Haftar announces conditional lifting of Libya oil blockade, Al Jazeera, 18 septiembre 2020.

- Libia: La ONU aplaude el acuerdo de alto el fuego y llama a alcanzar una solución política para un futuro de paz y seguridad, Noticias ONU, 23 octubre 2020.

- The National Oil Corporation lifts force majeure on Al Feel (The Elephant) Field and pleased to inform the entire Libyan people of the comprehensive ending of the blockades in all Libyan fields and ports, National Oil Corporation, 26 octubre 2020.

- Waha Oil Company’s production reduced by 200,000 BBLPD, cuenta NOC en Facebook, 17 enero 2021.

- Francia encabeza intervención aérea en Libia, Deutsche Welle, 19 marzo 2011.

- Biden has vowed to quickly restore the Iran nuclear deal, but that may be easier said than done, The Washington Post, 9 diciembre 2020.

- Resolución 2231 (2015), Consejo de Seguridad de la ONU, 20 julio 2015.

- The historic deal that Will prevent Iran from acquaring a nuclear weapon, Obama White House, 16 enero 2016.

- President Donald J. Trump Is Reimposing All Sanctions Lifted Under the Unacceptable Iran Deal, White House, 02 noviembre 2018.

- Monthly Oil Market Report, OPEP, 13 mayo 2016.

- Iran facts and figures, OPEP, 2020.

- Security Council Report, Twitter, 14 agosto 2020.

- Iran sanctions: Trump threatens to unilaterally reimpose UN measures, The Guardian, 20 agosto 2020.

- El Consejo de Seguridad de la ONU no actuará ante la petición de EE.UU. sobre las sanciones a Irán, EFE, 25 agosto 2020.

- Trump says Soleimani plotted ‘imminent’ attacks, but critics question just how son, Reuters, 03 enero 2020.

- Crisis nuclear de Irán: la controversial nueva ley de Teherán para restringir los controles a su programa nuclear, BBC Mundo, 03 diciembre 2020.

- Weekly Supply Estimates, Agencia de Información Energética de EE.UU., 13 enero 2020.

- From Keystone XL to Paris Agreement, Joe Biden signals a shift away from fossil fuels, CNN, 21 enero 2021.

- North America Rig Count, Baker & Houghes, 15 enero 2021.

- US banks prepare to seize energy assets as shale boom goes bust, Energy World, 10 abril 2020.

- ‘Stealth Bailout’ Shovels Millions of Dollars to Oil Companies, Financial Post, 15 mayo 2020.

- Haynes and Boone, LLP oil patch bankruptcy monitor, Haynes and Boone, 31 diciembre 2020.

- Cuatro muertos tras disturbios por seguidores de Trump en el Capitolio, Telemundo, 06 enero 2021.

- Impeaching Donald John Trump, President of the United States, for high crimes and misdemeanors, Congreso de EE.UU, 13 enero 2020.

- Biden immigration proposal looks to roll back four years of Trump’s hardline policies, USA Today, 20 enero 2021.

- Biden unveils $1.9 trillion economic and health-care relief package, The Washington Post, 14 enero 2021.

- Impeaching Donald John Trump, President of the United States, for high crimes and misdemeanors, Congreso de EE.UU, 13 enero 2020.

- Employment Situation Summary, Oficina de Estadísticas Laborales de EE.UU., 08 enero 2021.

- Las claves del RCEP, el mayor tratado de libre comercio del mundo (y cómo afecta a América Latina), BBC Mundo, 16 noviembre 2020.

- India to be fastest growing among major economies with growth rate of 9.72% in 2021, says GlobalData, Global Data, 18 enero 2021.

- Speech by President von der Leyen at the European Parliament Plenary on the inauguration of the new President of the United States and the current political situation, Comisión Europea, 20 enero 2021.

- El BCE pide una regulación global del bitcoin por tratarse de un activo “altamente especulativo”, El País, 13 enero 2021.

- Brexit | Viajar, estudiar, hacer negocios ¿Qué cambia a partir del 1 de enero de 2021?, EuroNews, primero enero 2021.

- Bailey Sees Stress Test Guiding Bank Payouts in 2021: BOE Update, Bloomberg, 06 enero 2021.

- Biden to sign 10 executive orders and invoke Defense Production Act to combat Covid pandemic , CNBC, 21 enero 2021.

- China’s COVID outbreak worst since March 2020, Reuters, 18 enero 2020.

- Weekly Stocks (crude & petroleum), Administración de Información Energética de EE.UU., 13 enero 2020.

- Weekly Stocks, Administración de Información Energética de EE.UU., 13 enero 2020.

- Weekly Stocks (crude oil SPR), Administración de Información Energética de EE.UU., 13 enero 2020.

- Weekly Supply Estimates, Administración de Información Energética de EE.UU., 13 enero 2020.

- Ganar menos de un dólar al mes en Venezuela, Euro News, primero octubre 2020.

- Refugiados y migrantes de Venezuela, Plataforma de Coordinación para Refugiados y Migrantes de Venezuela, 05 enero 2020.

- Presidente Maduro: tenemos la meta de producir 1 millón 500 mil barriles diarios, PDVSA, 15 enero 2021.

- Halliburton y Schlumberger ratifican compromiso con incremento de la producción petrolera, Aporrea, 29 septiembre 2017.

- PDVSA firmó acuerdo con empresas para incrementar producción de crudo, Ministerio de Petróleo de Venezuela, 28 agosto 2018.

- U.S. judge authorizes sale of Citgo parent shares despite Treasury ban, Reuters, 15 enero 2021.

- Gobierno acuerda pago de deuda con Crystallex para proteger a Citgo, El Estímulo, 26 noviembre 2020.

- Venezuela propone acuerdos que permitan a empresas privadas operar campos petroleros: fuentes, Reuters, 14 enero 2020.

- Esta es la Ley Antibloqueo con todos sus detalles, Banca y Negocios, 30 septiembre 2020.

- Guyana to export its first share of oil in coming days: oficial, Reuters, 12 febrero 2020. Arbitral award of 3 october 1899, Corte Internacional de Justicia, 18 diciembre 2020.